Australian Clinical Labs (ASX:ACL) – A Case Study Using My Personal Process

In this post I’ll use Australian Clinical Labs (ACL.AU) as a case study to walk through my basic investment process, which I’ve refined over the past thirty years to hone in on the types of companies I am looking for.

Previously, we looked at the 7 benefits of an investment process and how to build an effective investment process. So, we understand what benefits an Investment Process brings us, and also how to construct one that is effective without being exhaustive. What we need to do now is apply that Investment Process to get our desired result of better decisionmaking.

My investment process asks a series of questions:

- How does the company score on my Top Level Investment Factors?

- What sort of investment opportunity is available?

- What is the key factor for this investment and what does a more detailed review of this factor tell me?

- Why has the market has given me this opportunity?

- How does this investment compare to others?

- How do I execute?

Whilst there is a logical sequence to these questions, the reality is they are iterative. My process involves constantly looping between the questions to come to a conclusion.

In future pieces I’ll come back with more detail on each part of this process, but for the purposes of getting started, here is a quick runthrough.

How does ACL rate relative to my Top Level Investment Factors?

My process has eight top level factors or questions that I consider as a preliminary screen.

Balance Sheet – How Strong is the Company’s Balance Sheet?

Net debt excluding leases is ~$65m and current strong levels of profitability should see this reduce further. The main issue to consider is the large lease costs – which amount to ~16% of non-covid revenue.

Preliminary assessment = Good.

Earnings Quality – How well do reported earnings represent underlying economics?

No obvious earnings quality issues. Operating cash flow approximates EBITDA and there is minimal capex.

Preliminary assessment = Very Good.

Returns – Outlook for incremental returns?

Current Returns On Funds Employed appear to have been massively boosted by COVID. Assuming a return to baseline would not be pleasant. How long will margins persist, and how far will they fall post COVID?

Preliminary rating = Poor or Very Poor.

Governance – Quality of Management and Governance Structures and Incentives

Short term remuneration is based on EBITDA and long term targets on relative index performance. Both seem a bit generous given COVID tailwinds. Senior management also sold significant stakes into IPO.

Preliminary rating = Poor

Business – Quality of Business Franchise?

The pathology sector has solid long term growth – with an ageing population and new tests driving volume. This is offset by gradual declines in per unit pricing.

However, ACL is the third player in the Australian market. It is significantly smaller than the major players and whilst it has some in market scale in VIC/SA/WA , historically it has generated lower margins due to this lack of scale.

Preliminary rating = Good

Valuation

On valuation I ask two questions:

- What is the business worth in its current state?

- What might the business be worth in three years?

In both cases I’m looking for a rough idea of valuation. In this situation my preliminary assessment would be a valuation somewhere in the order of 1.5x sales (equivalent to 15x EBIT on 10% margins). With ex COVID sales of ~$600m this equates to approximately $900m enterprise value. Subtract some debt and add in some additional near term earnings from COVID and I get a preliminary valuation of around $1bn = ~$5/share. We’ll circle back to this number.

Preliminary Rating = Average

Momentum – What is the current trend of the operating business?

Momentum has been excellent due to the growth in testing due to COVID which has prompted a round of upgrades. However, as NSW and Vic outbreaks come back under control, testing volumes will likely taper and fall.

Preliminary rating = Very Good.

Overall:

In the vast majority of cases, this high level review fails to deliver a compelling investment thesis and I’ll park the idea until something changes. In this case the high level of current returns coupled with a valuation that looks sort of right would probably stop me from continuing.

Given I reach that conclusion by taking a lot of short cuts on the following steps, I’ll run though my thinking in more detail.

What sort of investment opportunity does ACL present?

Although every investment opportunity is unique – it helps when processing them to have a selection of categories available to highlight what are the more important questions to ask. For example Peter Lynch used six categories – Slow Growers, Stalwarts, Fast Growers, Cyclicals, Turnarounds, Asset Plays.

I use an abbreviated set of categories:

Deep Value – Buying existing assets cheaply

Cyclical – Expect return on existing capital to improve.

Growth – Ability to deploy capital at high incremental rates of return

(Earnings) Yield – Existing Cashflows will be re-rated to better reflect risk.

Special Situations – Takeover artbitrage/Liquidity trade etc..

For each category, the indicative relevance of each factor varies as follows:

| B. Sheet | Earn Q. | Returns | Gov. | Business | C. Val | F. Val | Mo. | |

| Deep Value | XXX | X | X | X | X | XXX | X | X |

| Cyclical | XX | X | XXX | X | XX | XX | X | XXX |

| Growth | XX | XX | XXX | XXX | XX | X | XXX | XXX |

| Yield | XX | XXX | XX | XX | XXX | XXX | X | X |

I would classify ACL as a cyclical investment – given the strong cyclical (i.e. non-permanent) boost provided by COVID. This suggests to me that the key factors to consider will be Returns and Momentum.

What are the key investment factors and what does a more detailed review of them tell me?

From our initial review it is clear that the key consideration for ACL is the impact of COVID:

Returns Factor – What are normalized margins post COVID? and

Momentum Factor – When is this likely to occur?

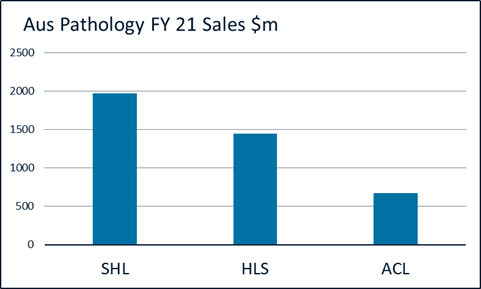

On the first question, my starting point is this chart.

Historically ACL has generated much lower margins than its peers due to its smaller scale. Given the very high incremental returns available from COVID testing (high prices) and its low starting base, ACL has been a relatively much bigger beneficiary of COVID than its peers.

It is clear that margins will fall post COVID – but by how much? It may not be all the way back to the low single digit margins that existed pre – COVID, due to some improved efficiencies and scale, but somewhere in the mid-high single digit range seems reasonable.

On this basis we could fine tune our valuations above to lock in 1.5x sales (15x EBIT @ 10% EBIT margins) as the upper end of valuations and a current valuation based on closer to 7-8% margins(or ~1.25x sales). This gives an approximate valuation range of $4.50 – $5.50.

The next question is that of Momentum. When will returns start to normalize? On this note whilst earnings might still be in upgrade mode, the underlying trend in COVID testing has already tipped in NSW and likely soon in Victoria.

On this basis I would review our preliminary assessment of Momentum from Very Good down to Average.

Why has the market given me this opportunity?

There is a famous saying in poker that if you have been playing for half an hour and still don’t know who the patsy is, then it’s you. In the case of ACL there are two ways to look at the opportunity:

“The market has underestimated the earnings leverage to higher testing volumes.” This argument was certainly true six months ago, but probably less so now.

“The market has underestimated the long term sustainable level of margins post COVID”. I don’t profess to know the exact level margins will settle at – although history suggests it is somewhere below current levels. But to make a committed investment at this point you need to have some conviction that your assessment of long term margins is better than the market’s.

How does this investment compare to others?

It is not enough that you have found a good investment. Is it the best use of your limited capital? Warren Buffet urges investors to think of having a limited lifetime dance card of investment to force this thinking.

I’ll confess that I get up on the investing dance floor a lot more than I should. One of the primary ways I use Blocks is to help me get some objective reference points for the relative strength of my ideas. This comes both in the score from my process but also regular screening against my other potential investments.

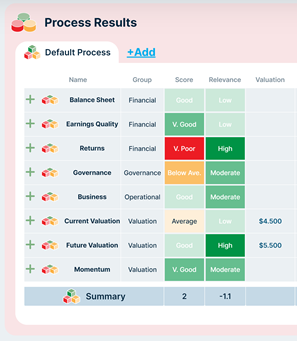

In the case of ACL the total score rates at a fairly neutral level (0), whilst the weighted score taking into account my assessment of Returns and Momentum as the Key Factors rates poorly (-3).

How to execute?

The final step in the investment process is how to execute your idea – when and how much to buy (or sell). Given ACL does not warrant a place on my current dance card – we will leave a discussion of this for a later date.

Conclusion

It’s easy to detail an investment process in logical steps, but the practical reality involves a combination of explicit analysis and implicit understanding that are iterated against each other in an endless loop.

Too much data and explicit analysis leads to a failure to understand the dynamic system you are investing in. You miss the wood for the trees. Too little and you risk crashing because you missed an obvious signal.

The best processes will combine these two attributes. A degree of rigour to avoid simple mistakes. A degree of flexibility to exploit the ideas between the cracks.

After 30 years I’m still learning and fine tuning my approach. I developed Blocks to help me add some rigour to how I assess the explicit analysis for my own investments. I hope you can find it a useful starting point in yours.

STAY IN TOUCH

Thanks for reading. Stay in touch by signing up for a free account on https://myblocks.app/. All users receive regular updates of our latest posts and deep dives on stocks. Alternatively, follow us on Twitter @myblocksapp.

ASX:ACL, Australian Clinical Labs